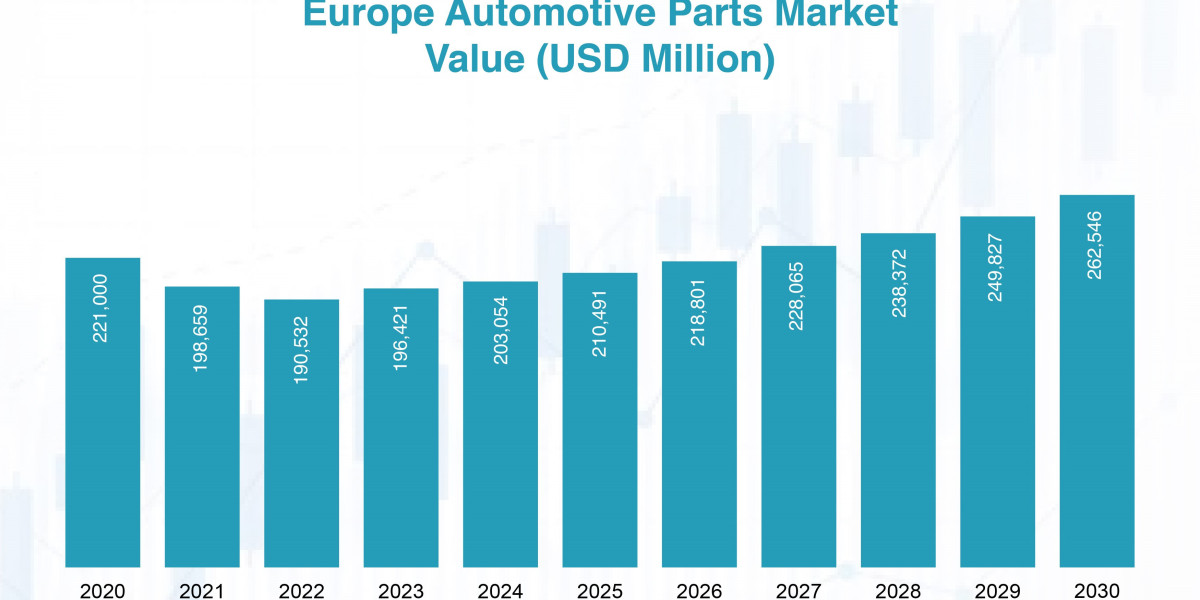

The Automotive Parts Market remains a fiercely contested arena where scale, technological capability, and regional footprint determine survival. Valued at USD 203,054 Million in 2024 and growing toward USD 262,546 Million by 2030 at 4.5% CAGR, the Europe Automotive Parts Market is led by a handful of giants who have successfully pivoted from mechanical to mechatronic dominance.

Bosch continues to hold the crown with roughly 12% overall share, thanks to its unmatched breadth in braking, powertrain electronics, and ADAS sensors. Continental follows closely at 10%, having transformed itself from a tire company into a leader in vehicle dynamics and automated driving software. ZF Friedrichshafen commands 8–9% through its world-class transmission and chassis technology, while Magna International and Valeo each secure 6–7% via body electronics, lighting, and thermal systems.

French giant Forvia (the merged Faurecia + Hella entity) has consolidated a strong 7% position in exhaust systems and interior modules, proving that traditional components can still thrive when re-engineered for hybrids and EVs. Emerging Chinese players such as CATL and BYD are rapidly gaining 3–5% share in battery systems and power electronics through aggressive localization and joint ventures, putting pressure on established European battery suppliers like Northvolt and Varta.